From Joint Center for Housing Studies of Harvard University

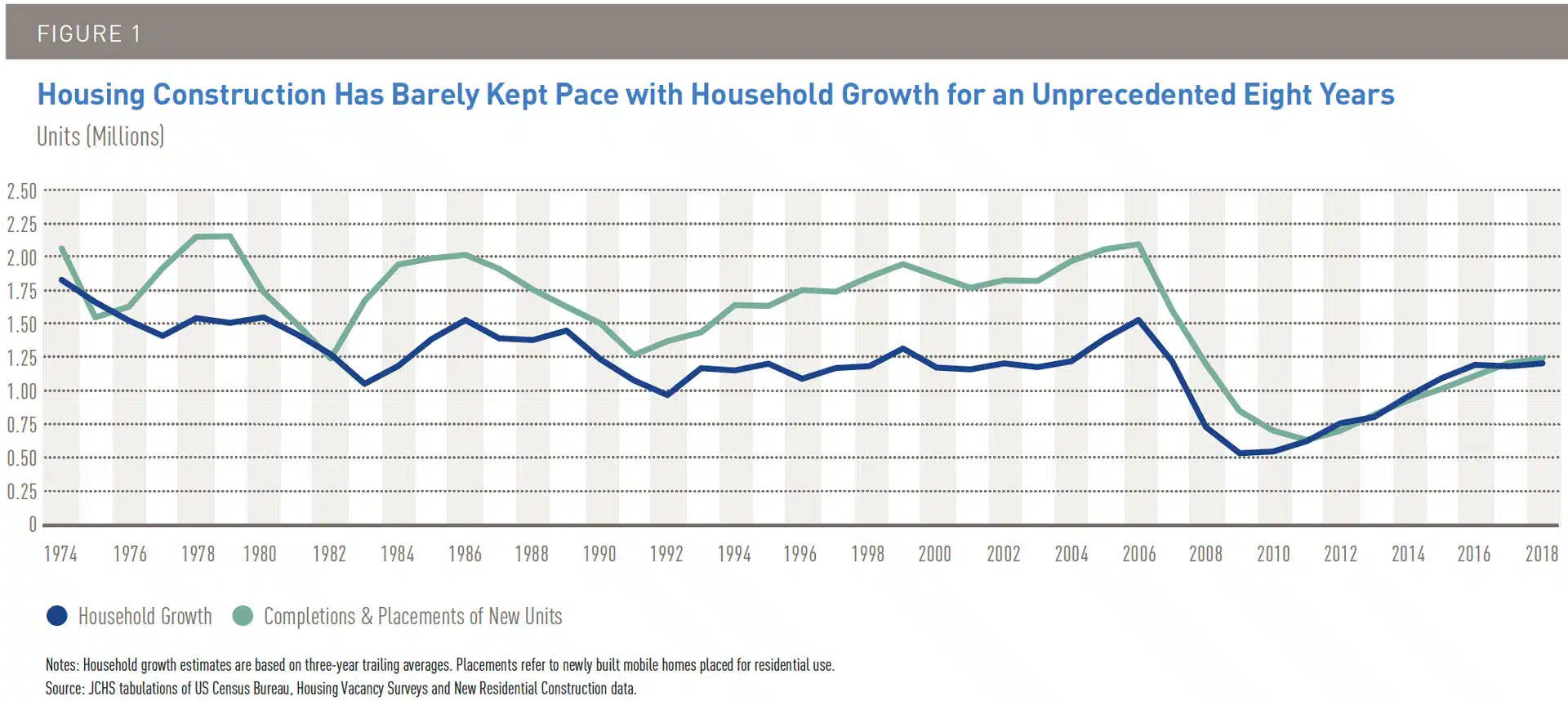

Just as the recent housing downturn was longer and deeper than any other since the Great Depression, the residential construction rebound has been slower. Since reaching bottom in 2011 at just 633,000 new units, additions to the housing stock have grown at an average annual rate of just 10 percent. Despite these steady gains, completions and placements totaled only 1.2 million units last year—the lowest annual production, excluding 2008–2018, going back to 1982.

The sluggish construction recovery is in part a response to persistently weak household growth after the recession. On a three-year trailing basis, the number of net new households dropped below 1.0 million in 2008 and held below that mark for seven straight years, including a low of just 534,000 in 2009. By comparison, even through the three recessions and large demographic shifts that occurred between 1980 and 2007, household growth still averaged 1.3 million annually and only dipped below 1.0 million once.

With the economy finally back on track, household growth picked up to 1.2 million a year in 2016–2018, close to expected levels given the size and age composition of the population. But new construction was still depressed relative to demand, with additions to supply just keeping pace with the number of new households (Figure 1). As a result, the national vacancy rate for both owner-occupied and rental units fell again in 2018, to 4.4 percent, its lowest point since 1994.

Although there have been brief periods when residential construction was similarly constrained, the duration of today’s tight conditions is unprecedented. Since 1974, annual additions to the housing supply exceeded household growth by an average of 30 percent to accommodate replacement of older housing, additional demand for second homes, population shifts across markets, and some slack for normal vacancies. According to Joint Center for Housing Studies estimates, annual construction should now be on the order of 1.5 million units, or about 260,000 higher than in 2018.